Context and Conceptual Scope

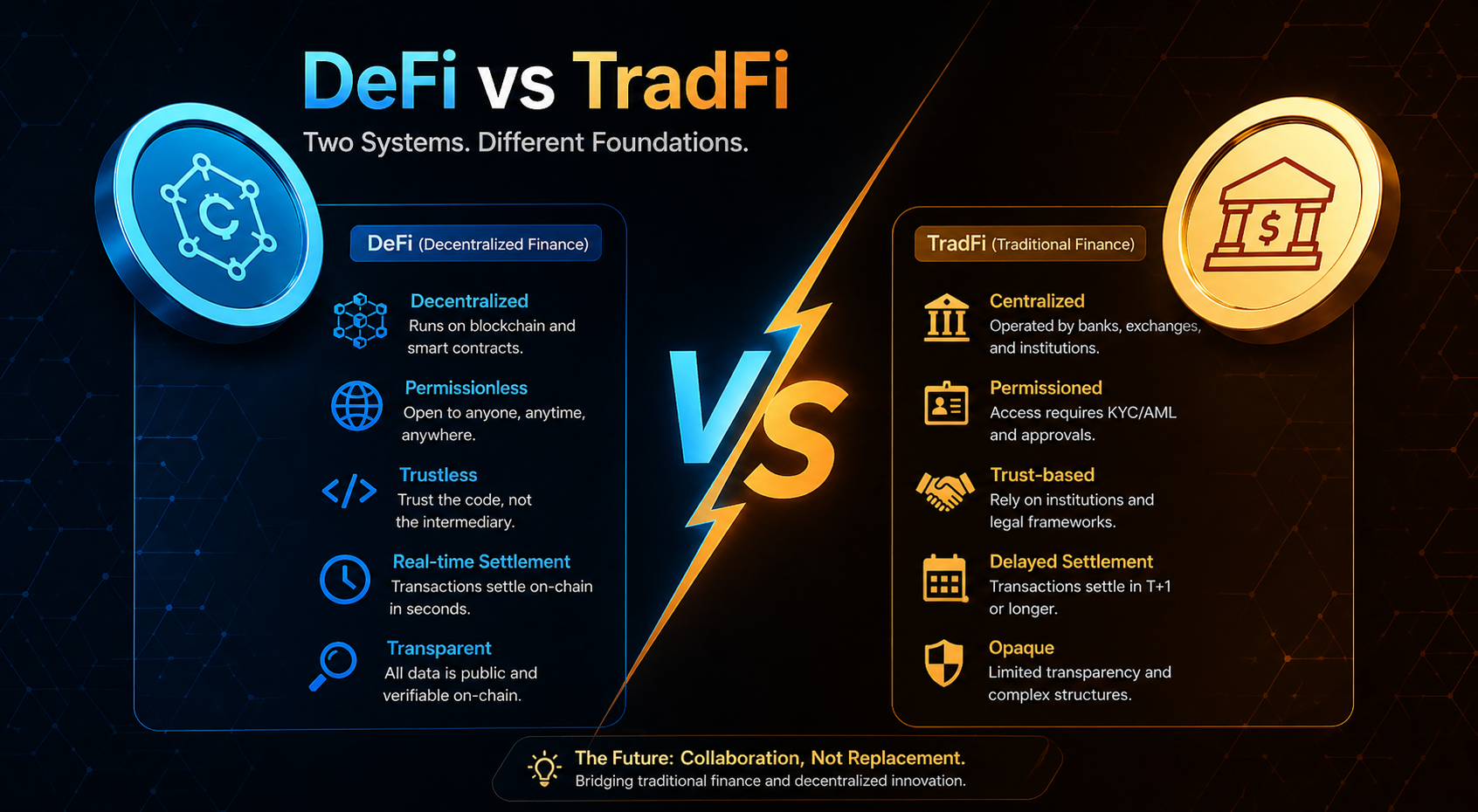

The term “TradFi” originates from the cryptocurrency ecosystem to distinguish traditional financial systems from decentralized finance (DeFi). From an institutional perspective, however, it represents a rebranding of the established financial framework, including banking, capital markets, payment systems, and regulatory bodies.

At its core, TradFi organizes economic activity through institutional trust, enabling efficient capital allocation across participants.

A Multi-layered Financial System

TradFi is a highly stratified system composed of multiple layers:

- Central banks, responsible for monetary policy (e.g., Federal Reserve)

- Commercial banks, providing deposits and loans (e.g., JPMorgan Chase)

- Investment banks, facilitating capital markets (e.g., Goldman Sachs)

- Stock exchanges, enabling price discovery (e.g., New York Stock Exchange)

- Payment networks, supporting settlement (e.g., Visa)

These entities collectively form an interconnected financial intermediary system.

Operational Mechanisms: Credit Intermediation and Settlement

The operation of TradFi can be understood through two key mechanisms: credit intermediation and settlement systems.

Banks act as intermediaries, transforming deposits into loans while managing risk. Transactions are finalized through clearing and settlement systems, often involving central counterparties (CCPs).

Settlement typically follows T+1 or T+2 cycles, enhancing stability but introducing counterparty risk and liquidity constraints.

Risk Control and Oversight

A defining feature of TradFi is its strong regulatory environment. Financial activities are governed by capital requirements, anti-money laundering (AML) rules, and know-your-customer (KYC) procedures.

Regulation aims to mitigate systemic risk and prevent financial crises. Historical events, such as the 2008 global financial crisis, have significantly shaped modern regulatory frameworks.

Institutional and Legal Foundations

Unlike DeFi, which relies on code and consensus, TradFi operates on institutional trust. Participants rely on banks, clearinghouses, and legal systems rather than directly trusting counterparties.

This model provides:

- Accountability through legal enforcement

- Intervention capability by regulators

- Stability based on established systems

Efficiency and Limitations

While TradFi offers stability and scale, it also has inherent limitations.

Centralization can reduce efficiency, especially in cross-border transactions requiring multiple intermediaries. Access barriers exclude unbanked populations, and opaque fee structures further limit transparency.