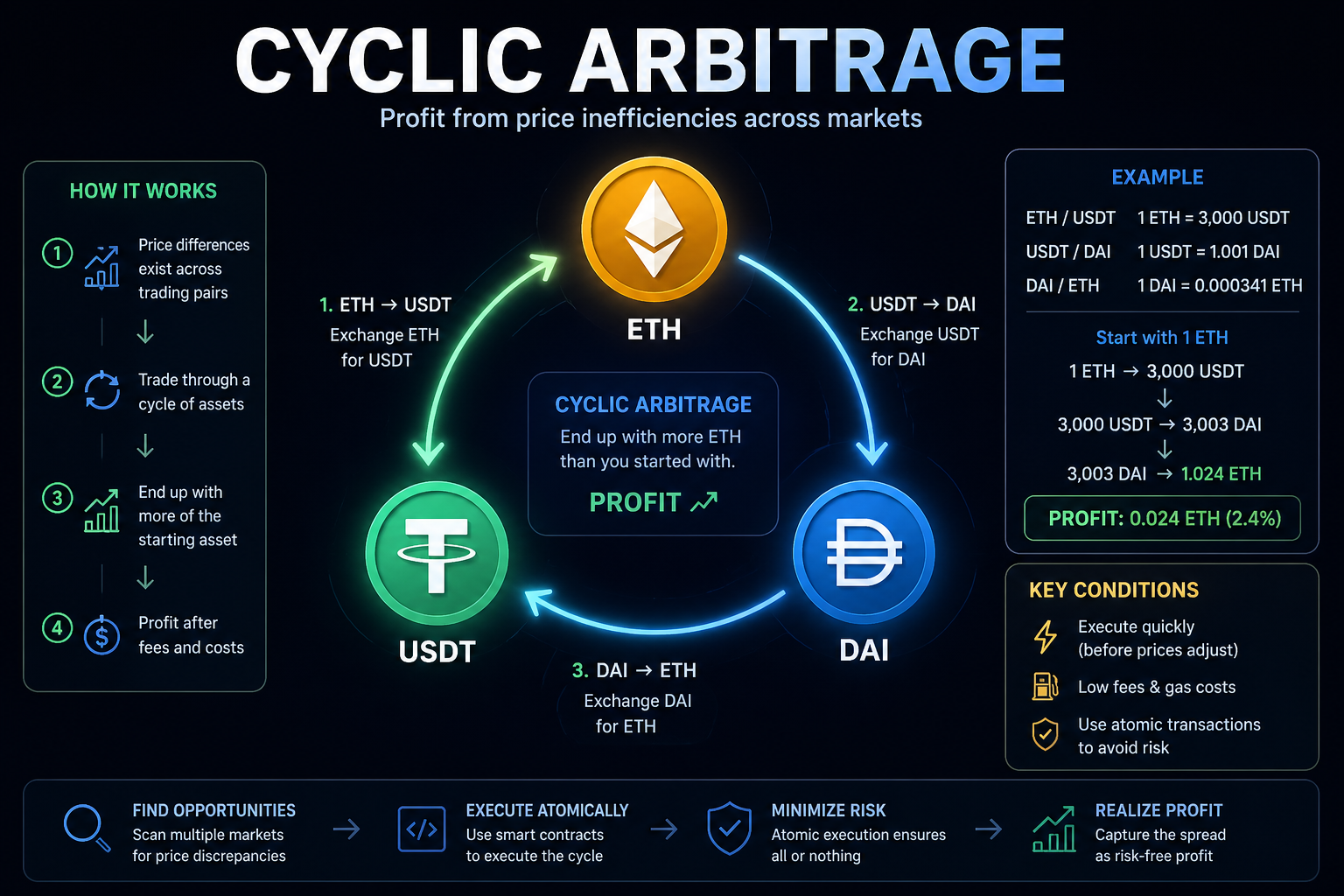

With the rapid expansion of decentralized finance (DeFi), triangular arbitrage has emerged as one of the most fundamental trading strategies in the crypto ecosystem. At its core, triangular arbitrage exploits price inconsistencies across multiple trading pairs. A trader starts with one asset, performs a sequence of swaps across different markets, and eventually returns to the original asset. If the final amount exceeds the initial input, a profit is realized. This mechanism is particularly common in decentralized exchanges, where prices are determined independently across multiple liquidity pools rather than through a centralized order book.

In automated market maker (AMM) systems such as Uniswap, asset prices are governed by mathematical formulas rather than bid-ask matching. The most widely used model is the constant product formula, which ensures that the product of the reserves remains constant after each trade. Since each liquidity pool updates its pricing independently based on trades occurring within it, temporary discrepancies naturally arise between different pools. These discrepancies form the foundation of arbitrage opportunities.

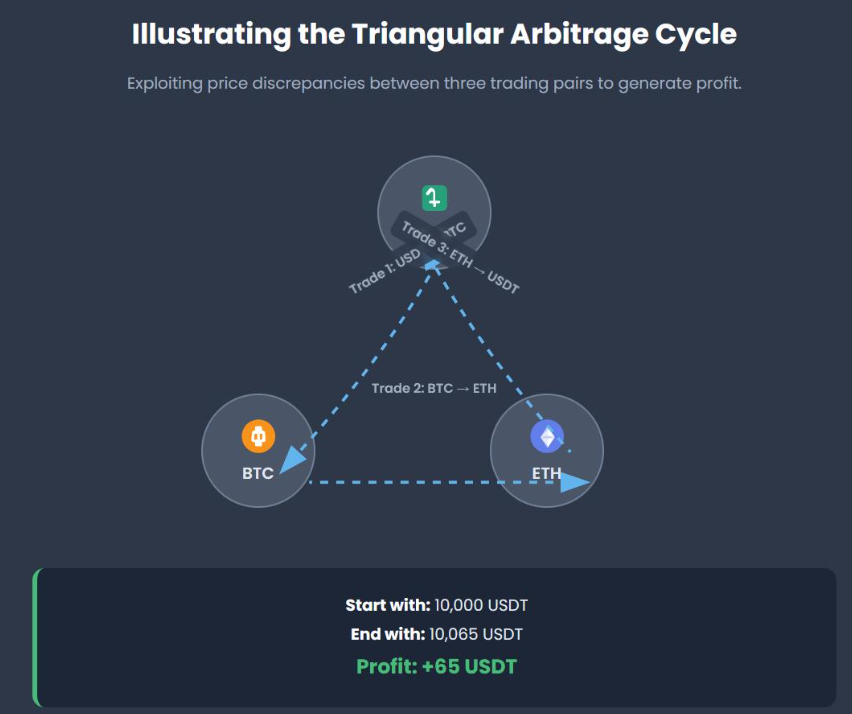

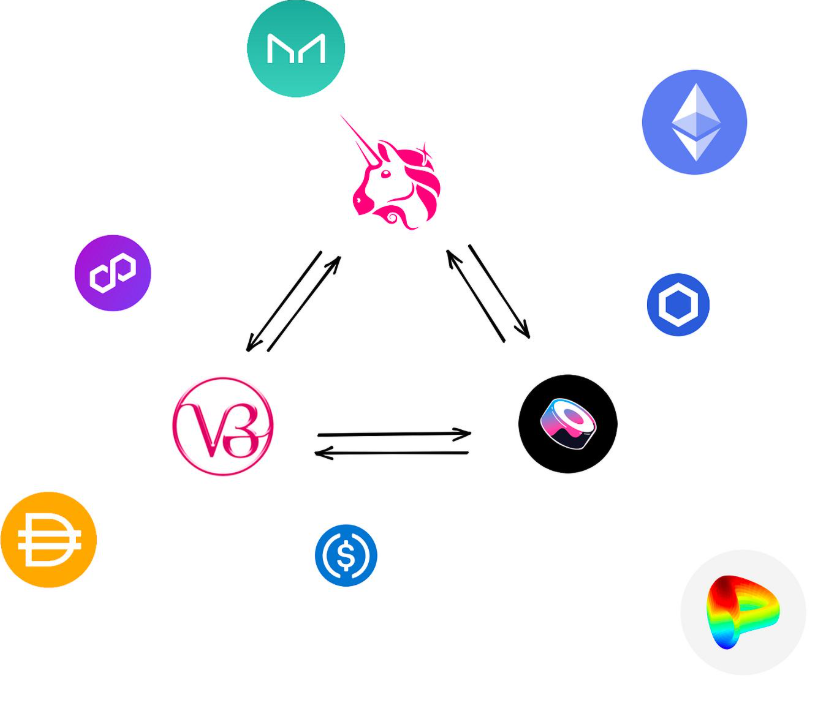

A typical triangular arbitrage involves three tokens. A trader might swap token A for B, then B for C, and finally C back to A. If the cycle results in more A than initially invested, the difference represents profit. Empirical evidence shows that such opportunities are not merely theoretical. In one documented case, a trader converted approximately 285 USDC through a sequence of swaps and ended up with over 303 USDC, generating a significant return . This profit is derived entirely from pricing inefficiencies rather than market direction。

From a theoretical standpoint, arbitrage profitability depends on whether the product of exchange rates along the cycle exceeds the cumulative trading fees. In AMM systems, each swap incurs a fee, which must be accounted for when evaluating profitability. According to the research, arbitrage opportunities only exist when the combined exchange rate product surpasses the fee-adjusted threshold . This explains why many apparent opportunities fail to yield profit once transaction costs are included.

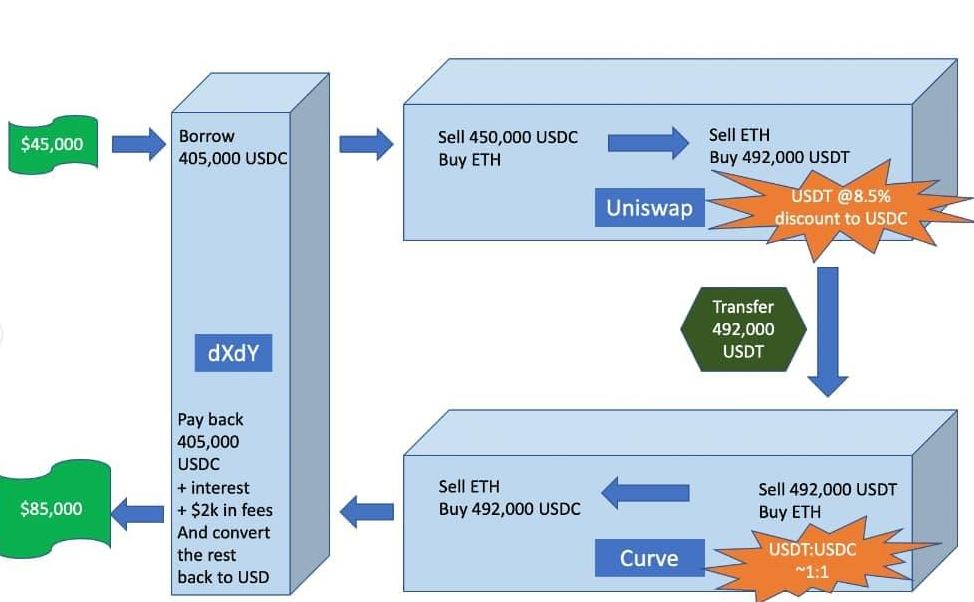

Although the concept of triangular arbitrage appears straightforward, its execution in real markets is highly sophisticated. Modern arbitrageurs rely on smart contracts to bundle the entire trading sequence into a single atomic transaction. This ensures that all steps are executed simultaneously; if the final outcome is not profitable, the transaction is reverted automatically. This approach significantly reduces exposure to price volatility and front-running attacks. In fact, the vast majority of arbitrage transactions in decentralized exchanges are executed in this atomic manner

From a market perspective, triangular arbitrage represents a substantial economic activity within DeFi. Studies show that over a period of less than a year, more than 292,000 cyclic arbitrage transactions were executed, generating over 138 million USD in revenue . Despite this large volume, many profitable opportunities remain unexploited, indicating that decentralized markets are not perfectly efficient. At the same time, high gas fees and intense competition from MEV bots significantly reduce the accessible profit margin, making this strategy viable primarily for technically advanced participants.

In conclusion, triangular arbitrage is more than just a trading strategy; it is a window into how decentralized markets function. It highlights the fragmented nature of liquidity, the dynamics of on-chain pricing, and the critical role of smart contracts in financial automation. For traders and developers alike, understanding cyclic arbitrage provides valuable insight into both market behavior and the underlying mechanics of DeFi systems.