Direct Market Access (DMA) extends the concept of remote trading access to brokerage clients. Its origins can be traced back to the 1980s, with early platforms such as Instinet leading the way. Although some institutional participants adopted DMA at an early stage, retail traders were in fact among the primary users. It is evident that vendors at the time actively targeted the retail segment with their DMA solutions. In modern markets, day traders—often referred to as “SOES bandits,” a term derived from NASDAQ’s Small Order Execution System—have gained unprecedented levels of control and access over their order flow.

During the 1990s, institutional interest in DMA grew significantly, particularly among hedge funds and statistical arbitrage firms. Early DMA offerings were largely provided by software vendors and smaller brokerage firms. However, around the turn of the millennium, major investment banks and broker-dealers began to invest heavily in this space. For instance, Goldman Sachs acquired REDIPlus in 2000; Bank of America Securities acquired Direct Access Financial Corp. in 2004; Sonic Trading Management was acquired by the Bank of New York; and Lava Trading became part of Citigroup. As a result, the DMA landscape quickly consolidated under major brokers and evolved into a key component of institutional trading services.

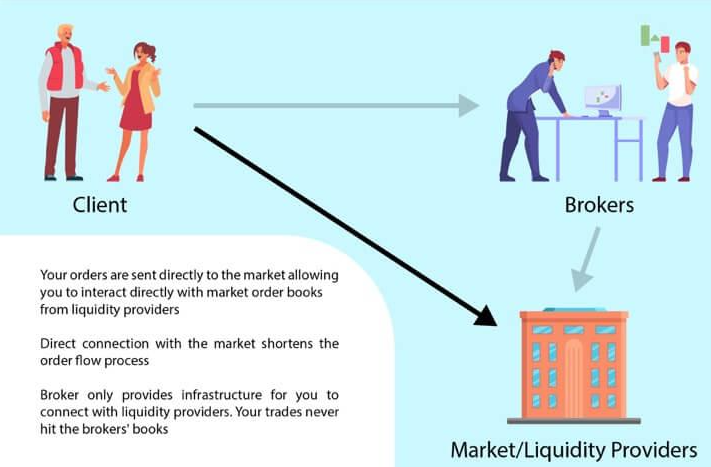

Under the DMA framework, clients leverage the broker’s infrastructure to route orders directly to exchanges, in much the same way as the broker’s proprietary orders. This gives rise to the concept of “zero-touch execution,” whereby clients retain full control over order submission and execution, without manual intervention from the broker. To operate effectively in this environment, traders must utilize an Order Management System (OMS) or Execution Management System (EMS), both of which are integrated with the broker’s systems. Prime brokerage services typically handle post-trade processes, including clearing, settlement, custody, and financing arrangements.

Information leakage remains a critical concern for institutional users. Consequently, DMA services are often operated as segregated entities within brokerage firms to ensure that client order flow is not visible to other trading desks—particularly proprietary trading divisions—thereby preserving confidentiality and maintaining execution integrity.