Introduction

In modern electronic markets, order types play a critical role in determining execution efficiency and risk management. A stop limit order combines a trigger mechanism with a price constraint, making it a widely used tool in both trading strategies and risk control. Compared to simple market or limit orders, it introduces a more sophisticated execution logic along with unique advantages and limitations.

Basic Structure

A stop limit order consists of two key parameters:

- Stop Price : the trigger level that activates the order

- Limit Price : the price constraint applied after activation

Before the stop price is reached, the order remains inactive and does not participate in the market. Once triggered, it becomes a limit order and is submitted to the order book.

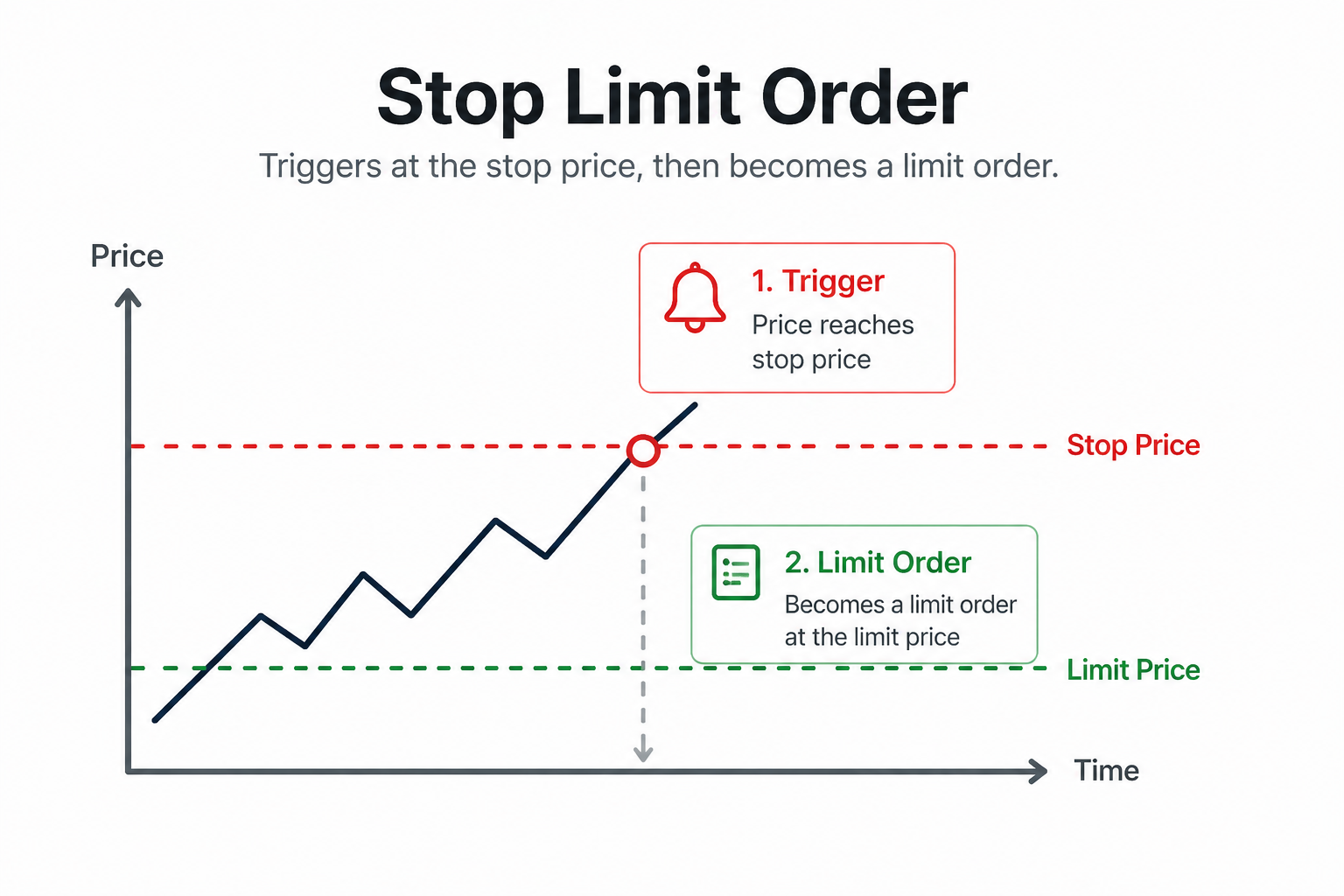

Execution Logic

The execution of a stop limit order can be understood as a two-stage process. Initially, the order remains dormant until the market price reaches the stop level. Once triggered, it is converted into a limit order and placed in the order book for execution.

For instance, if the market price is 100 and a trader sets a stop price at 105 and a limit price at 106, the order will only be activated when the price reaches 105. After activation, it will attempt to execute at 106 or better. If the market jumps directly to 107, the order may not be filled.

Use Cases: Buy and Sell

In buy scenarios, stop limit orders are often used to enter positions during upward breakouts. In sell scenarios, they are commonly used for risk management, triggering a sell order when the price falls below a certain threshold.

This dual mechanism allows traders to respond to market movements while maintaining control over execution prices.

Comparison with Stop Orders

A key distinction exists between stop limit orders and stop orders. A stop order becomes a market order upon activation, ensuring execution but not price certainty. In contrast, a stop limit order becomes a limit order, providing price control but no guarantee of execution.

This reflects a fundamental trade-off in trading: execution certainty versus price certainty .

Risks and Limitations

The primary risk of a stop limit order is non-execution. In fast-moving or illiquid markets, prices may gap beyond the specified limit, leaving the order unfilled.

Such scenarios are particularly relevant during high volatility periods or major market events, where liquidity conditions can change rapidly.

Microstructure Perspective

From a market microstructure perspective, stop limit orders are not visible in the order book prior to activation, making them a form of latent liquidity. Once triggered, they become standard limit orders and enter the price-time priority queue.

Clusters of stop orders can generate significant order flow upon activation, often leading to rapid price movements. This mechanism contributes to phenomena such as breakouts and flash crashes.