Now that the big picture is set, it is time to dive more deeply into the detailed mechanics of trading in modern financial markets. As we will see, practical

aspects of market design can substantially affect the microscopic-scale behaviour of individual agents. These actions can then proliferate and cascade to the macroscopic scale.

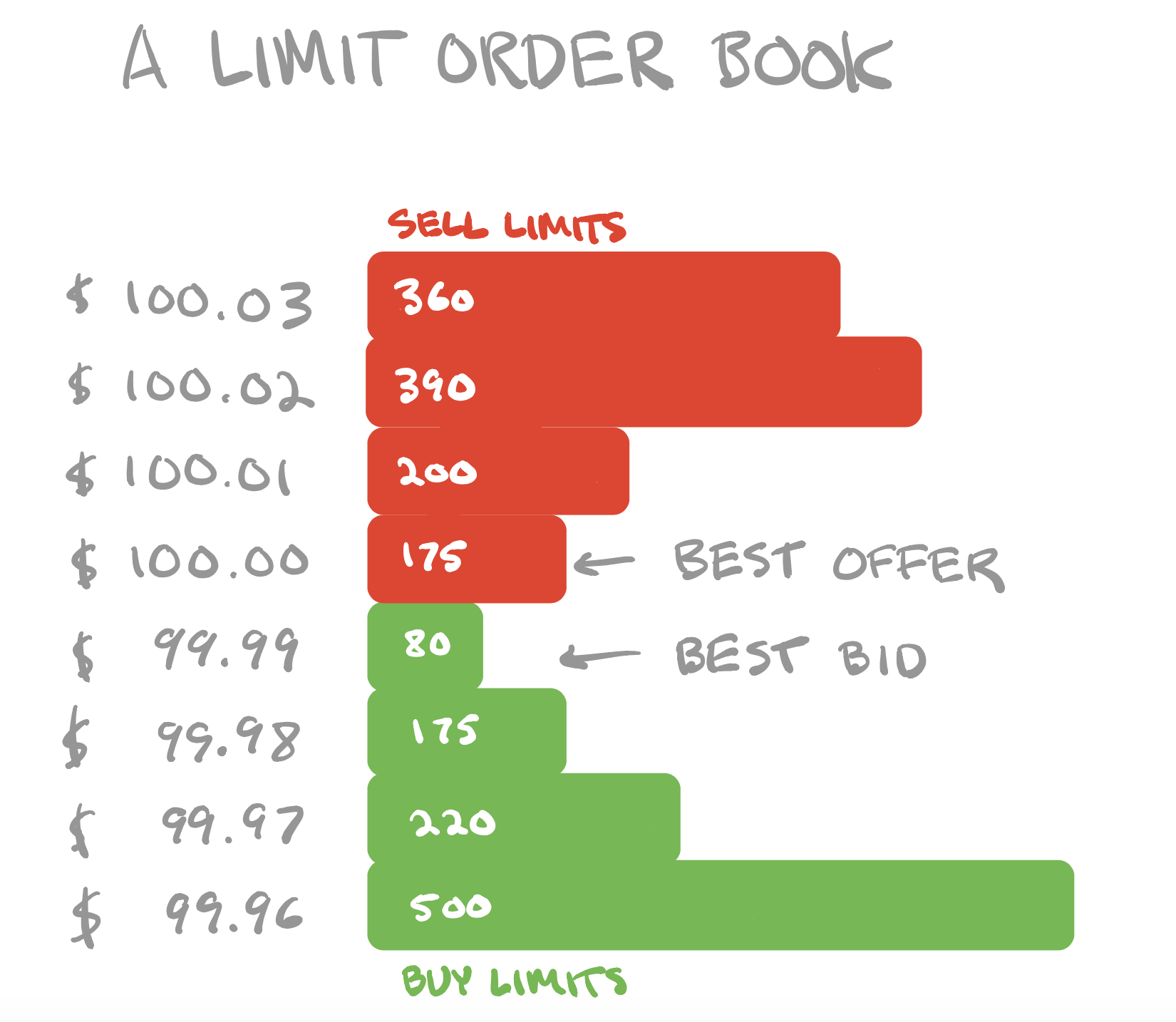

In this part, we will embark on a detailed discussion of limit order books (LOBs), which are nowadays omnipresent in the organisation of lit markets (i.e. open markets where supply and demand are displayed publicly). We will start by describing the founding principle of LOBs, namely the interaction between limit orders, which offer trading opportunities to the rest of the world, and market orders, which take these opportunities and result in immediate transactions. LOBs are not only a place where buyers meet sellers, but also a place where patient traders (or “liquidity providers”) meet impatient traders (or “liquidity takers”). For practical reasons, LOB activity is constrained to a predefined price and volume grid, whose resolution parameters are defined by the tick size and the lot size , respectively. At any point in time, the state of an LOB is defined by the outstanding limit orders on this grid.

LOBs are an elegant and simple way to channel the trading intentions of market participants into a market price. In an LOB, any buy and sell orders whose prices cross are matched and immediately removed from the LOB. Therefore, an LOB is a collection of lower-priced buy orders and higher-priced sell orders, separated by a bid–ask spread. The persistent aspect of limit orders is key for the stability of the LOB state and the market price.

Today, most of the world’s financial markets use an electronic trading mechanism called a limit order book (LOB) to facilitate trade. The Helsinki, Hong Kong,

London, New York, Shenzhen, Swiss, Tokyo, Toronto and Vancouver Stock Exchanges, together with Euronext, the Australian Securities Exchange and NASDAQ, all use LOBs, as do many smaller markets. In this chapter, we provide a detailed introduction to trading via LOBs, and we discuss how price changes in an LOB emerge from the dynamic interplay between liquidity providers and liquidity takers.